Get cannabis-specialized accounting that tracks profit by product, integrates with your POS, and gives you CFO-level guidance—so you can make confident decisions and maximize your margins.

We'll help audit-proof your Ohio dispensary, stay 280E compliant, and seamlessly integrate cost accounting with your Metrc tracking and cannabis POS systems—so you can focus on growth, not compliance headaches.

Work with us for Ohio cannabis expertise in America's newest market: day-one Metrc compliance, proper 280E structure, POS integration—without untested internal teams, Columbus premiums, or costly new-operator mistakes.

We love helping Ohio dispensaries and cannabis companies establish perfect cannabis accounting, 280E compliance, and real profit tracking while ensuring complete tax compliance.

If you're searching for a cannabis CPA in Ohio, you're operating in one of America's newest adult-use cannabis markets. Ohio launched recreational cannabis sales in August 2024, transforming from a medical-only program into a full adult-use market that industry analysts project will reach $1 billion annually within three years. This explosive growth opportunity affects dispensaries from Columbus to Cleveland, Cincinnati to Toledo, and throughout the Buckeye State where 11.8 million residents now have legal access to cannabis. Unlike established markets where operators learned through trial and error, Ohio cannabis businesses have the advantage of implementing best practices from day one—if they work with specialized accounting expertise. Your Ohio dispensary operates under Ohio Metrc seed-to-sale tracking (implemented since August 2017 for medical, now covering adult-use), faces IRS Section 280E federal tax restrictions identical to all U.S. cannabis businesses, and needs technology integration between your Dutchie POS or Cova system and accounting software. Most traditional Ohio CPAs either refuse cannabis clients or lack specialized knowledge to properly structure 280E-compliant cost accounting while maintaining Metrc reconciliation. Whether you're an established Ohio medical dispensary transitioning to dual-license operations or a new entrant capitalizing on adult-use legalization, you need an Ohio cannabis accounting specialist who understands the complete financial and regulatory ecosystem of the cannabis industry.

Ohio's August 2024 launch created a unique market dynamic where operators can avoid mistakes that plagued early-stage markets in Colorado, California, and Washington. Ohio cannabis businesses don't need to navigate tracking system transitions—Metrc has been Ohio's seed-to-sale platform since 2017, meaning infrastructure is stable and POS integration is mature. Ohio dispensaries benefit from established best practices: proven POS systems like Flowhub, Treez, BLAZE, and others already have deep Metrc integration. Cannabis banking, while still federally restricted, has evolved—Ohio operators can access Shield Compliance and other cannabis-friendly financial services that didn't exist when Colorado pioneered legalization in 2014. However, Ohio's new market also faces challenges: intense competition as established medical operators (who received first priority for adult-use licenses) now compete with new entrants; price compression as supply increases faster than demand in the market's early months; and operational inexperience among dispensary teams who haven't navigated the complexities of high-volume retail operations, inventory management, and compliance requirements. The most critical advantage Ohio operators have is the opportunity to implement proper accounting infrastructure from day one. Specialized Ohio cannabis CPAs help new operators establish chart of accounts designed for 280E compliance, set up cost accounting methodology that maximizes COGS capitalization, integrate POS systems with QuickBooks or Xero properly, and build product-level profitability tracking from first sale forward. Getting this right initially costs less and delivers better results than trying to clean up six months of incorrect bookkeeping done by generic accountants who don't understand cannabis.

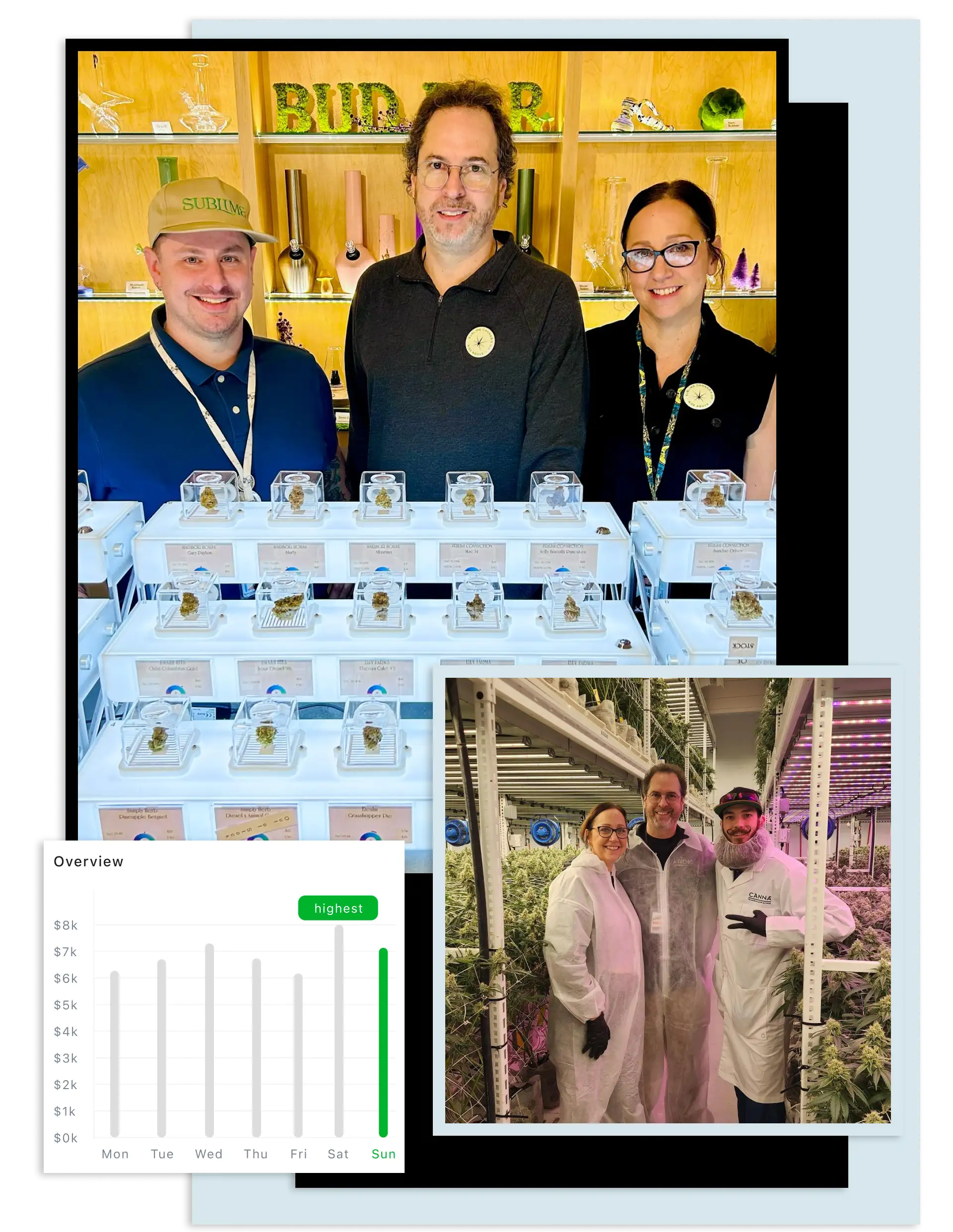

Ohio implemented Metrc in August 2017 for its medical cannabis program, giving the state over seven years of operational experience before adult-use launch. Metrc uses RFID tagging technology where every cannabis plant receives a unique 24-digit identifier that follows the product from cultivation through processing, laboratory testing, packaging, distribution, and retail sale. When Ohio dispensaries receive inventory from cultivators or processors, those products arrive with Metrc package tags. Your POS system must scan these tags during retail sales, deducting inventory from Metrc's tracked database and recording the transaction. Here's where accounting becomes critical: your financial records must reconcile perfectly with Metrc inventory data. If your QuickBooks shows you sold $450,000 worth of flower in November but Ohio Metrc reflects $447,500, you have a discrepancy. That $2,500 gap could represent inventory shrinkage (loss, theft, or damage), compliance violations (sales not properly recorded in Metrc), accounting errors (incorrect revenue recognition), or data integration problems between your POS and accounting software. Each explanation has different implications—some are normal business operations, others are regulatory red flags. Specialized Ohio cannabis bookkeeping includes monthly Metrc reconciliation procedures: comparing financial system inventory balances to Metrc package tracking, investigating and documenting all discrepancies, and maintaining audit trails proving inventory continuity. This monthly discipline ensures you're perpetually audit-ready when Ohio Division of Cannabis Control conducts compliance reviews or when acquisition opportunities emerge requiring clean financial due diligence.

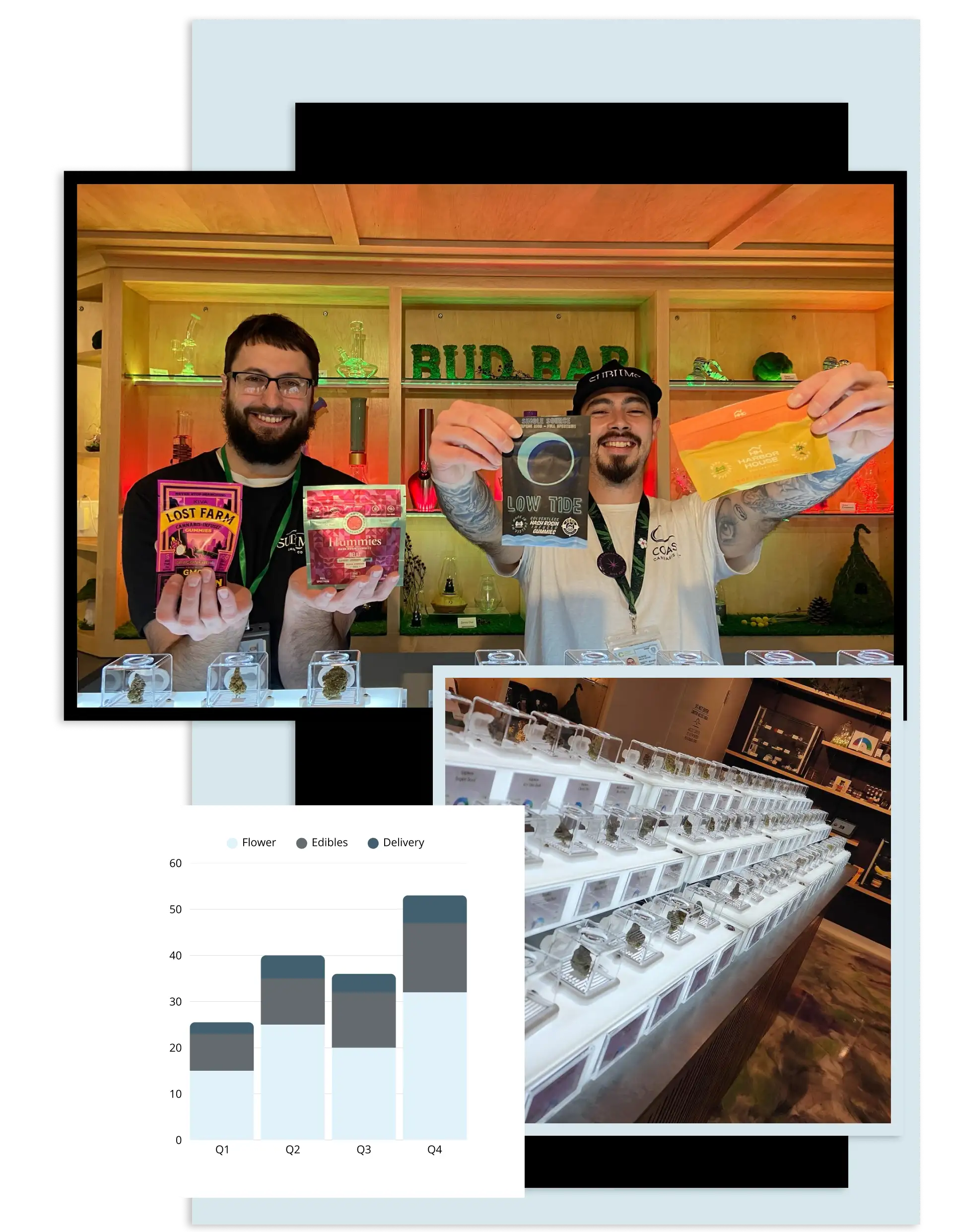

Ohio's mature Metrc infrastructure means dispensaries have numerous proven POS options with established integration. The dominant platforms in Ohio include Dutchie POS, offering full Metrc integration with Retail ID support and growing market share among Ohio operators; Flowhub, which aggressively marketed its Metrc expertise to Ohio dispensaries and claims first-mover advantage in cannabis POS; Treez, providing cloud-based multi-location capabilities important for operators planning Columbus and Cleveland expansion; Cova Software, which developed specific compliance features for Ohio's regulatory requirements; and BLAZE, targeting high-volume dispensaries in Ohio's urban markets. Beyond POS selection, Ohio operators must integrate ecommerce and delivery platforms. Jane, Leafly, and Weedmaps drive customer discovery and online ordering, but each platform charges fees (typically 8-15% of sales or monthly subscriptions) that dramatically impact channel economics. Many Ohio dispensaries make the mistake of chasing revenue across all available channels without analyzing true profitability after platform fees and attributable costs. Sophisticated Ohio cannabis accounting establishes chart of accounts tracking revenue by product type (flower, pre-rolls, vape cartridges, edibles, concentrates, topicals) and by sales channel (in-store, Jane, Leafly, Weedmaps, Dutchie delivery, direct ecommerce). Monthly financial statements reveal product-level gross margins and channel-level net revenue after fees, enabling data-driven decisions about product mix optimization and marketing allocation. This operational intelligence creates sustainable competitive advantage—while competitors chase vanity metrics like total revenue or customer count, you're optimizing for actual profitability and return on invested capital in Ohio's rapidly evolving cannabis marketplace.

Ohio's new adult-use operators—especially those without medical cannabis experience—frequently make catastrophic 280E errors during their first year. IRS Section 280E prohibits cannabis businesses from deducting ordinary operating expenses, allowing only Cost of Goods Sold deductions. Common mistakes Ohio dispensaries make include treating 280E as a tax-season problem instead of a daily operational requirement (cost accounting must happen in real-time, not reconstructed annually); deducting rent, utilities, and facility costs as operating expenses instead of allocating them proportionally to cultivation, processing, or retail spaces and capitalizing qualifying portions into COGS; failing to capitalize labor costs for employees who touch inventory—budtenders, inventory managers, cultivation workers should be capitalized into product costs; taking marketing and advertising deductions despite explicit 280E prohibition (even grand opening expenses and Leafly advertising are non-deductible); deducting delivery driver wages and vehicle expenses as transportation costs instead of capitalizing delivery labor into COGS; and attempting creative entity structures like separate "management LLCs" or "consulting companies" that tax courts have consistently rejected. Ohio operators influenced by advice from non-cannabis CPAs frequently hear "just set up a management company"—this doesn't work and exposes you to IRS challenges. Proper Ohio cannabis accounting requires cannabis-specific expertise, monthly review of expense classifications to ensure proper capitalization, documentation proving cost allocation methodology for shared facility expenses, and separation of truly non-plant-touching revenue (branded merchandise, rolling papers) that isn't subject to 280E restrictions. Specialized Ohio cannabis CPAs implement these procedures from day one, ensuring your first tax return is correct rather than requiring costly amended returns when mistakes are discovered.

Ohio cannabis businesses face tax burdens that shock operators unfamiliar with 280E economics. A dispensary generating $4 million in annual revenue with 50% gross margin ($2 million gross profit) faces approximately $1.2-1.4 million in federal tax liability—60-70% effective tax rate on gross profit. Add Ohio state corporate income tax, sales tax obligations, and local taxes, and your total tax burden reaches $1.3-1.5 million annually. Many Ohio operators underestimate this liability because they're accustomed to traditional business taxation where 21% federal corporate rate applies. Cannabis operators lose most deductions, creating dramatically higher effective tax rates. This demands aggressive cash flow management: setting aside 30-35% of monthly revenue for quarterly federal estimated tax payments, maintaining cash reserves covering 3-4 months of tax obligations, budgeting for annual tax preparation and potential audit defense, and planning for the gap between when revenue is earned (and taxed) versus when cash is collected from credit card processors or delivery platforms. Ohio dispensaries that fail to budget properly face catastrophic cash crunches during quarterly estimated payment deadlines. Fractional CFO services for Ohio cannabis businesses include quarterly tax planning sessions reviewing estimated payments, cash flow forecasting projecting tax obligations across upcoming quarters, and strategic guidance on entity structure, owner compensation, and reinvestment decisions that optimize after-tax cash flow. This proactive tax management prevents the panic-driven mistakes Ohio operators make when caught unprepared: taking emergency loans at predatory rates, missing tax deadlines and incurring penalties, or pulling funds from operations and damaging business growth. Getting tax planning right from launch separates sustainable Ohio cannabis businesses from those that generate revenue but fail financially.

The optimal time for Ohio dispensaries to engage cannabis-specialized accounting is during license application and facility buildout—before generating first dollar of revenue. Early engagement ensures your accounting infrastructure, chart of accounts, cost accounting procedures, and technology integrations are established correctly from day one. Many Ohio operators try to save money initially by using generic bookkeepers or handling accounting themselves, then discover six months into operations that their books are wrong, 280E compliance is incorrect, and they need specialized firms to reconstruct historical records while maintaining current operations. This costs more than implementing proper systems initially and creates unnecessary risk during Ohio Division of Cannabis Control audits. If you're already operating, the second-best time is immediately—before tax season creates deadline pressure, before compliance issues compound, and while there's time to implement proper systems and possibly file amended returns if necessary. Ohio cannabis accounting specialists can audit your current setup, identify mistakes, and implement corrective procedures. Ohio's cannabis market is new but maturing rapidly—larger operators, private equity, and multi-state operators are already evaluating Ohio acquisition opportunities. Specialized accounting ensures you're always ready to raise capital, respond to partnership offers, or refinance debt because your financials are pristine, your 280E compliance is defensible, and your business intelligence demonstrates operational excellence that commands premium valuations. Getting accounting right from the start positions your Ohio dispensary for long-term success in what analysts predict will become one of America's largest cannabis markets—the Buckeye State's 11.8 million residents and central geographic location create opportunity that sophisticated operators with proper financial infrastructure will dominate while underprepared competitors struggle with back-office chaos that undermines their operational potential.

Cannabis & 280E Tax & Accounting Specialist.

Adam Drust CPA

CannaDrust CPA